Most Popular

-

6

[KH Explains] How should Korea adjust its trade defenses against Chinese EVs?

![[KH Explains] How should Korea adjust its trade defenses against Chinese EVs?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/15/20240415050562_0.jpg&u=20240415144419)

-

7

BTS' Jungkook creates Instagram account for his dog

-

8

Korea braces for blows from Middle East conflict

-

9

S. Korea ups guard against economic impact from Middle East conflict

-

10

Guterres urges maximum restraint after Iranian assault on Israel

![[KH Explains] How should Korea adjust its trade defenses against Chinese EVs?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/15/20240415050562_0.jpg&u=20240415144419)

[Future of Plastic Cards] With digital payments rising, will plastic cards become things of past?

Fast-changing market trends led by technology require card behemoths to be adaptable

By Kim Young-wonPublished : July 26, 2020 - 15:58

This is the first installment in a series of articles and interviews assessing the future of credit cards as a major payment platform and challenges ahead. -- Ed.

The rapid growth of mobile payment services is offering wider options for customers, but for the South Korean credit card industry it is both an opportunity and threat.

Some naysayers even predict the demise of plastic credit cards that replaced cash payments for years. Fears linger over the possible emergence of a Korean-version of China’s widely popular Alipay -- mobile and online payment platform established by Alibaba Group. However, the entry of tech giants in the market could be a catalyst for change for credit card issuers, experts say.

“The overall market conditions are not that favorable for credit card companies for now as the government has been maintaining strict regulations on traditional player, while digitalization is changing the market landscape,” said Yoo Chang-woo, a senior official at Visa Korea’s consulting and analytics division, at a conference held earlier this month in Seoul.

“Card companies are in a critical juncture to prove whether they can adapt to the new business environment,” he added, quoting Charles Darwin’s theory of biological evolution that it is not the strongest species that survives, but one that is most adaptable to change.

A number of digital payment solutions have been mushrooming in the nation in recent years -- such as Kakao Pay and N Pay, which are operated by tech behemoths Kakao and Naver, respectively.

Armed with convenient services and plentiful benefits, digital payment systems are gradually grabbing more share in the overall payment market long dominated by credit card operators. Since the mobile solutions do not require users to carry a bunch of physical cards, they are garnering immense popularity among young people while posing a threat to conventional card issuers.

The Korean government’s strict regulations for the traditional financial industry as well as its persistent drive to reduce credit card fees also make related firms lose their competitive edge with tech savvy mobile payment services operators that are subject to more lenient rules.

Since 2016, credit card processing fees for purchases at small businesses have been cut from 1.5 percent to 0.8 percent as part of the government’s move to reduce financial burden on the public. The lower fees, however, have been undermining the profits of card issuers, hampering them to invest in cutting-edge big data and artificial intelligence technologies for online services, and to acquire companies that can help beef up their tech capability.

The rapid growth of mobile payment services is offering wider options for customers, but for the South Korean credit card industry it is both an opportunity and threat.

Some naysayers even predict the demise of plastic credit cards that replaced cash payments for years. Fears linger over the possible emergence of a Korean-version of China’s widely popular Alipay -- mobile and online payment platform established by Alibaba Group. However, the entry of tech giants in the market could be a catalyst for change for credit card issuers, experts say.

“The overall market conditions are not that favorable for credit card companies for now as the government has been maintaining strict regulations on traditional player, while digitalization is changing the market landscape,” said Yoo Chang-woo, a senior official at Visa Korea’s consulting and analytics division, at a conference held earlier this month in Seoul.

“Card companies are in a critical juncture to prove whether they can adapt to the new business environment,” he added, quoting Charles Darwin’s theory of biological evolution that it is not the strongest species that survives, but one that is most adaptable to change.

A number of digital payment solutions have been mushrooming in the nation in recent years -- such as Kakao Pay and N Pay, which are operated by tech behemoths Kakao and Naver, respectively.

Armed with convenient services and plentiful benefits, digital payment systems are gradually grabbing more share in the overall payment market long dominated by credit card operators. Since the mobile solutions do not require users to carry a bunch of physical cards, they are garnering immense popularity among young people while posing a threat to conventional card issuers.

The Korean government’s strict regulations for the traditional financial industry as well as its persistent drive to reduce credit card fees also make related firms lose their competitive edge with tech savvy mobile payment services operators that are subject to more lenient rules.

Since 2016, credit card processing fees for purchases at small businesses have been cut from 1.5 percent to 0.8 percent as part of the government’s move to reduce financial burden on the public. The lower fees, however, have been undermining the profits of card issuers, hampering them to invest in cutting-edge big data and artificial intelligence technologies for online services, and to acquire companies that can help beef up their tech capability.

Although credit cards have had numerous customers with big transactions for decades, they were short of utilizing the treasure trove of data. It was presumably because they were too noble or lazy to put their hands on a myriad of unorganized data sets. Instead of building their own technical competitiveness, they have often chosen to collaborate with tech companies.

Experts, however, warned they could lose their ground to emerging mobile payment services providers if they fail to keep up with changing market trends.

“For now, having partnerships with tech-driven mobile payment services firms is inevitable, but the traditional card companies would lose their leadership in the payment segment in a long run if they do not enhance their own competitiveness,” Park Tae-joon, head of a research unit under the Credit Finance Association of Korea, an organization that represents local credit card companies, wrote in a recent report.

Data also show that an increasing number of people are turning to mobile payment solutions for money transfer and online purchases instead of using credit cards. The average number of payments made per day via the mobile systems last year stood at 6 million, up from 1 million in 2016 and 4.8 million in 2016, according to the Bank of Korea.

Not dead yet

Although traditional card issuers face a number of difficulties, some market officials forecast that plastic cards will not easily become obsolete.

“When the market saw digitalization trends, such as mobile payments, for the first time some years ago, many talked about the end of the credit card, but the conventional payment method has survived and will do so for a while as personal preference of credit cards and mobile payment services differs, between generations in particular,” an official from a local card firm said.

Not to lag behind, card issuers have been making efforts to launch new services and technologies while partnering with companies in different sectors.

Shinhan Card, the nation’s largest credit card issuer, has launched different services to enable smartphone users to easily make purchases online and offline.

One of those services is a payment system utilizing sound waves. A sound wave transmitter that can be attached to the back of a smartphone body allows credit card holders to pay for their purchases via point of sale terminals installed at stores and restaurants. The payment device is compatible not only with Android phones but also Apple’s iPhones. Although Apple Pay, the US phone maker’s signature mobile payment system, is not available in the nation, iPhone users here can make offline payments thanks to the sound wave device.

In addition to the sound wave-based payment solution, Shinhan has been testing facial recognition technology for payment at retail stores in a local university campus in Seoul. Amid the coronavirus pandemic, such contactless payments have been receiving more spotlight recently than before, according to a Shinhan Card official.

“Creative thinking and ideas do not necessarily mean they will create something totally new, but will connect things in our daily lives and expand them in different realms,” said Woo Sang-su, a big data unit leader at Shinhan Card, adding the company tries to offer highly tailored services based on its data analytics tech.

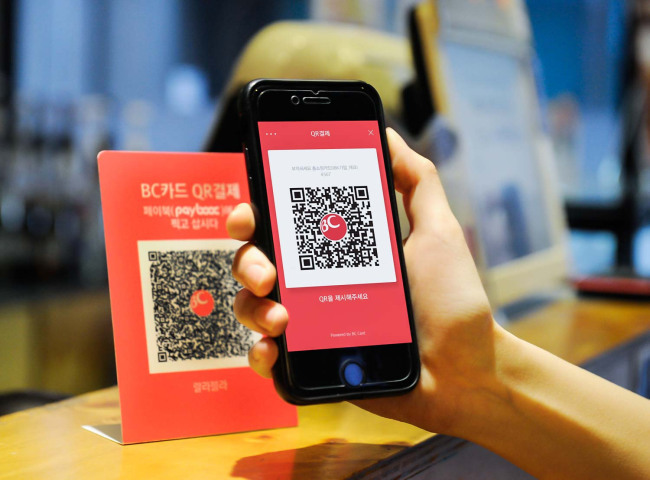

QR codes are another sought-out payment method here. Payment processing firm BC Card in particular has been nurturing the QR code payment solution, which allows a card holder to pay for purchases by scanning the QR code on a smartphone. Its Paybooc QR solution is available at some 45,000 convenient stores run by top five convenience store chains -- GS25, CU, 7-Eleven, Emart24, and Ministop. BC Card has been working with local card companies to standardize the QR code system while collaborating with peers in China and Vietnam to enable cross-border QR code payments.

Hyundai Card, on the other hand, has been trying to expand its territory via partnerships in different sectors. As part of that scheme, it has been rolling out private label credit cards, which are designed to offer benefits for customers of specific brands and stores.

The card company, for instance, plans to launch a credit card that offers a Starbucks drink for customers who have collected a certain amount of mobile stamps on the coffee house’s application. Food delivery service Baedal Minjok, car-sharing service Socar and Korean Air are some companies that are, or will soon be, in partnership with Hyundai Card for such a tailored credit card.

By Kim Young-won (wone0102@heraldcorp.com)

Experts, however, warned they could lose their ground to emerging mobile payment services providers if they fail to keep up with changing market trends.

“For now, having partnerships with tech-driven mobile payment services firms is inevitable, but the traditional card companies would lose their leadership in the payment segment in a long run if they do not enhance their own competitiveness,” Park Tae-joon, head of a research unit under the Credit Finance Association of Korea, an organization that represents local credit card companies, wrote in a recent report.

Data also show that an increasing number of people are turning to mobile payment solutions for money transfer and online purchases instead of using credit cards. The average number of payments made per day via the mobile systems last year stood at 6 million, up from 1 million in 2016 and 4.8 million in 2016, according to the Bank of Korea.

Not dead yet

Although traditional card issuers face a number of difficulties, some market officials forecast that plastic cards will not easily become obsolete.

“When the market saw digitalization trends, such as mobile payments, for the first time some years ago, many talked about the end of the credit card, but the conventional payment method has survived and will do so for a while as personal preference of credit cards and mobile payment services differs, between generations in particular,” an official from a local card firm said.

Not to lag behind, card issuers have been making efforts to launch new services and technologies while partnering with companies in different sectors.

Shinhan Card, the nation’s largest credit card issuer, has launched different services to enable smartphone users to easily make purchases online and offline.

One of those services is a payment system utilizing sound waves. A sound wave transmitter that can be attached to the back of a smartphone body allows credit card holders to pay for their purchases via point of sale terminals installed at stores and restaurants. The payment device is compatible not only with Android phones but also Apple’s iPhones. Although Apple Pay, the US phone maker’s signature mobile payment system, is not available in the nation, iPhone users here can make offline payments thanks to the sound wave device.

In addition to the sound wave-based payment solution, Shinhan has been testing facial recognition technology for payment at retail stores in a local university campus in Seoul. Amid the coronavirus pandemic, such contactless payments have been receiving more spotlight recently than before, according to a Shinhan Card official.

“Creative thinking and ideas do not necessarily mean they will create something totally new, but will connect things in our daily lives and expand them in different realms,” said Woo Sang-su, a big data unit leader at Shinhan Card, adding the company tries to offer highly tailored services based on its data analytics tech.

QR codes are another sought-out payment method here. Payment processing firm BC Card in particular has been nurturing the QR code payment solution, which allows a card holder to pay for purchases by scanning the QR code on a smartphone. Its Paybooc QR solution is available at some 45,000 convenient stores run by top five convenience store chains -- GS25, CU, 7-Eleven, Emart24, and Ministop. BC Card has been working with local card companies to standardize the QR code system while collaborating with peers in China and Vietnam to enable cross-border QR code payments.

Hyundai Card, on the other hand, has been trying to expand its territory via partnerships in different sectors. As part of that scheme, it has been rolling out private label credit cards, which are designed to offer benefits for customers of specific brands and stores.

The card company, for instance, plans to launch a credit card that offers a Starbucks drink for customers who have collected a certain amount of mobile stamps on the coffee house’s application. Food delivery service Baedal Minjok, car-sharing service Socar and Korean Air are some companies that are, or will soon be, in partnership with Hyundai Card for such a tailored credit card.

By Kim Young-won (wone0102@heraldcorp.com)